Fertilizer Shock: The Chokepoint That Will Feed This Year's Food Inflation

Brent at $110 made the front page. Urea at $700 will make the grocery bill.

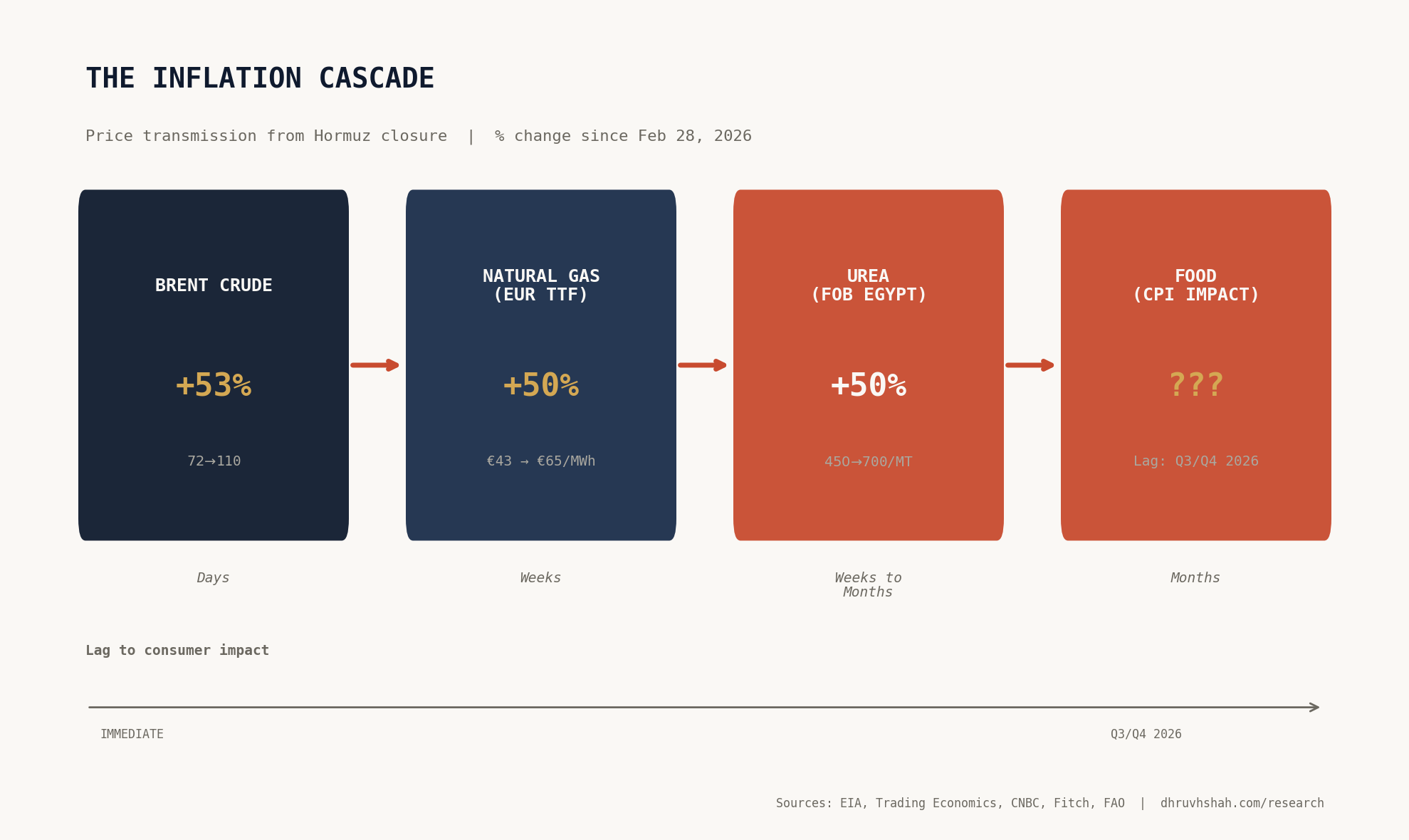

- 1Urea hit $700 per ton. A third of global fertilizer ships through Hormuz. Oil has a pipeline workaround. Fertilizer does not. Spring planting is happening right now.

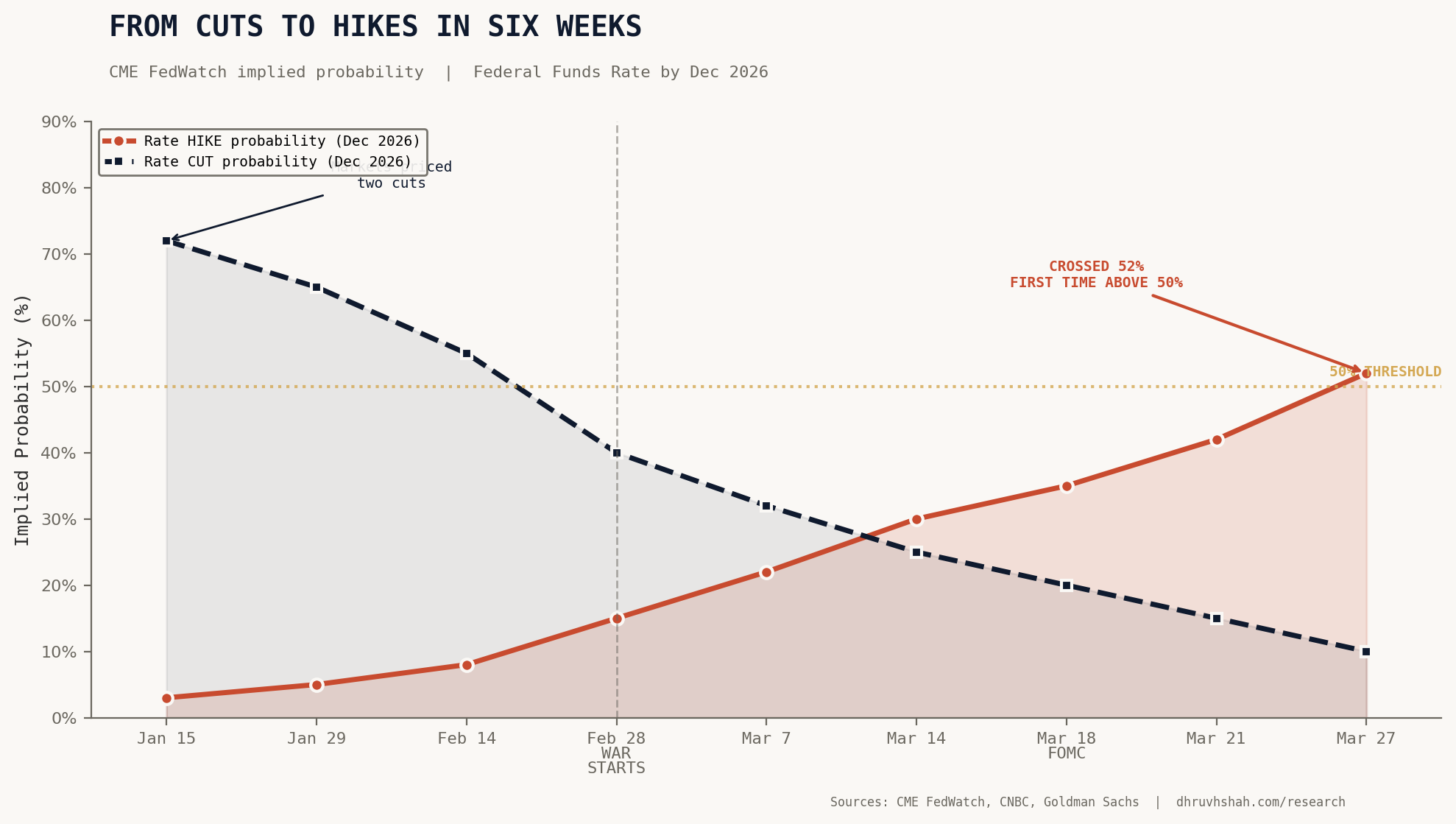

- 2Fed funds futures crossed 52% probability of a rate hike by December on Friday. Six weeks ago, the market was pricing two cuts. The fastest policy expectations reversal since 2022.

- 3The Dow entered correction territory. The Nasdaq is 13% off its October high. But the real repricing has not started. The fertilizer to food pipeline runs on a three to six month lag. What goes in the ground this April shows up on the shelf in October.

The Chokepoint That Feeds the World

Everyone knows Hormuz carries 20% of the world's oil. Fewer people know it carries a third of globally traded fertilizer. That distinction matters because oil has workarounds. Saudi Arabia pipes crude to Yanbu. The U.S. has a strategic petroleum reserve. The IEA released 400 million barrels.

Fertilizer has none of that. No strategic urea reserve. No ammonia pipeline to a western port. The Gulf accounts for roughly 43% of seaborne urea exports, and every ton ships through Hormuz. FOB granular urea out of Egypt has jumped from around $450 per metric ton before the war to roughly $700 today. That is not a spike. That is a regime change.

Planting Season Does Not Wait

Corn farmers across the U.S. Midwest are making nitrogen application decisions right now. Miss the window and yields drop. The American Farm Bureau Federation warned the White House last week that corn production faces a catastrophic moment, with diesel above $5 per gallon and fertilizer costs doubled.

Early USDA projections suggest a historic shift in acreage from nitrogen intensive corn toward soybeans, which fix their own nitrogen. Rational for individual farmers, terrible for aggregate food supply. Corn feeds livestock, becomes ethanol, and is embedded in processed food from cereal to soda. Less corn planted this spring means tighter supply by Q4.

The supply response that would normally cap the spike is not coming. Russia suspended ammonium nitrate exports in March to protect its own planting. Egypt's production capacity has been halved because Israeli gas fields that feed its plants went offline. Fitch raised its 2026 urea price expectations by 25%. And both Middle Eastern maritime corridors are now compromised simultaneously. Hormuz is closed to Western flagged shipping. The Houthis have resumed Red Sea attacks. Saudi Arabia's Yanbu pipeline bypass routes tankers directly through Houthi missile range. Roughly 140 container ships remain stranded in the Gulf. Maersk has suspended Suez transits again.

The Fed Trap

A supply shock that simultaneously raises prices and slows growth is the worst scenario for monetary policy. Powell said at the March FOMC that the Fed historically looks through oil shocks. But the textbook was written for shocks that resolve in weeks, not for a conflict entering its second month with no offramp.

The data is moving faster than the committee. Import prices jumped 1.3% in February, the largest monthly gain since March 2022. The OECD raised its U.S. inflation forecast to 4.2%, well above the Fed's 2.7% projection. Seven FOMC members have dots showing no cuts this year. The 2 year yield spiked nearly 60 basis points in a single week to 3.96%. The bond market is not pricing a temporary disruption. It is pricing a durable inflation shock.

On Friday, CME FedWatch showed 52% implied probability of a rate hike by December, the first time above 50%. By Monday it retreated to 14%. Goldman called the spike an overshoot. They may be right about the direction. But the speed of the repricing tells you something: the consensus that this war is a short term disruption is breaking down.

What It Means for Equities

The S&P's fifth straight weekly decline is not capitulation. It is a slow repricing for a world where the Fed cannot cut and might have to hike. Energy is the only sector posting gains in March. But the second order trades matter more.

CF Industries and Mosaic are directly exposed to the nitrogen squeeze. Consumer staples face input cost pressure that will not show up until Q3 earnings. Airlines are caught between fuel costs they cannot hedge at these levels and demand they cannot reprice fast enough. And the entire growth trade gets worse if the 10 year pushes above 4.50%.

What to Watch

If Iran's selective transit policy expands beyond Chinese and Indian flagged vessels by mid April, the fertilizer squeeze eases faster than expected. Watch for any UN brokered humanitarian corridor that includes bulk commodity shipping, not just food aid.

If the USDA's March 31 Prospective Plantings report shows corn acreage below 88 million acres, the nitrogen substitution trade is confirmed and the food inflation pipeline is loaded.

If the 10 year yield breaks 4.50% and holds, the equity correction has another leg down.

And if tanker transits through Bab al Mandeb fall below the already suppressed levels of the past week, the Saudi Yanbu workaround fails and the market loses its last pressure valve.

Everyone is watching the oil price.

They should be watching the planting season.

You can replace a barrel of crude. You cannot replace a missed growing window.

For informational purposes only. Not investment advice. Sources: EIA, USDA, CME FedWatch, OECD, Reuters, American Farm Bureau Federation, Fitch, Wall Street Journal. Prices as of 4:00 PM ET, March 27, 2026.