The Private Markets Boom Is Real. But the Easy Money Phase Is Over.

VanEck BDC Income ETF

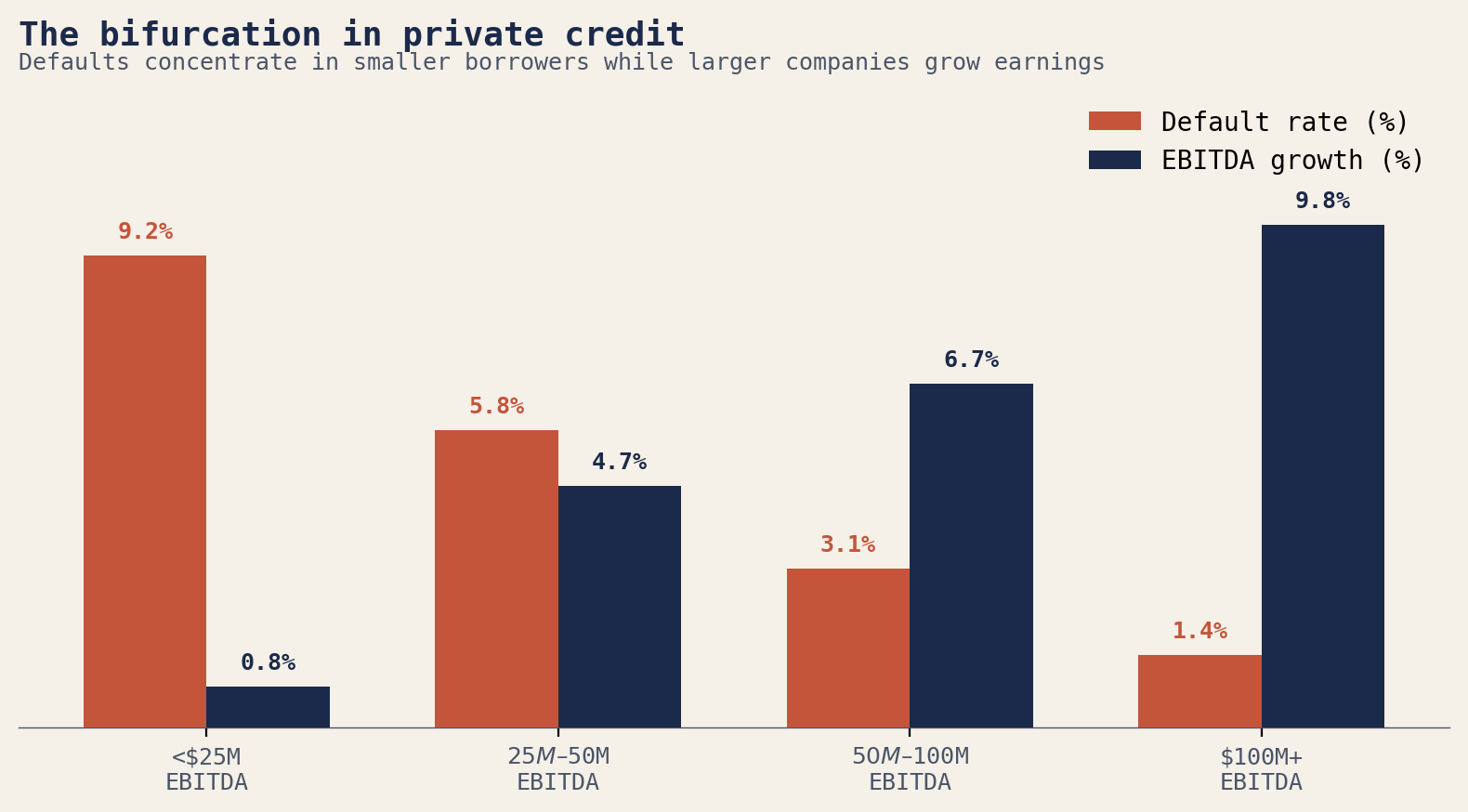

The U.S. private credit default rate is 5.8% or 1.4%, depending on where you look. That gap says more about private markets in 2026 than any headline about trillion dollar deal years ever could. Private credit and private equity are both bigger and more fragile than they have ever been. And the macro environment that powered their rise is not coming back.

Two markets, one liquidity problem

Private credit has grown from roughly $2 trillion in 2020 to $3.5 trillion today. Private equity deal value crossed $1.2 trillion in 2025, the second highest year on record. These are no longer separate stories. Private credit finances most PE deals under $1 billion. The secondaries market ($240 billion in volume last year, up 48%) exists because both asset classes share the same problem: too much capital stuck in place with no clean way out.

The growth was a product of a specific macro setup. Post 2008 bank regulations pushed traditional lenders out of middle market lending. Years of near zero rates made private credit yields look exceptional. When the Fed hiked in 2022 and 2023, floating rate loans got even more attractive since yields moved up with SOFR. The asset class won on both sides of the rate cycle.

That is unwinding now. The Fed cut 100 basis points between September and December 2024, giving some relief to stressed borrowers. But rates are still well above the decade before 2022, and the pause on further cuts has left overleveraged companies stuck. Spreads have tightened as capital floods in, compressing the yield premium that drew investors in the first place.

In PE, buyout deals above $500 million topped $1 trillion in 2025, eclipsing 2021. The $55 billion take private of Electronic Arts set an all time record. PE backed IPOs raised $62 billion, up from $8 billion two years prior. But the recovery was narrow. Tariff uncertainty caused a sharp pullback in Q2 2025, and 40% of GPs cited geopolitical risk as a drag on cross border activity. The H2 rebound was driven by a handful of megadeals, not broad confidence.

The bifurcation nobody talks about

The macro pressure is not landing evenly. That is the most important thing to understand right now.

Fitch's U.S. private credit default rate hit 5.8% through January 2026, the highest on record. In its privately monitored universe, the rate reached 9.2%. Consumer products defaults nearly doubled to 12.8%. Healthcare remains the most stressed sector. Payment in kind usage, where borrowers defer cash interest and roll it into principal, crept to 11% from 7% in 2021.

Now look at the upper middle market. Borrowers with $100 million plus in EBITDA have covenant default rates of just 1.4%, below the five year average, and are growing earnings at nearly 10%. They have pricing power and the scale to absorb tariff exposure and input cost inflation. The smaller borrowers do not. Many of those loans were written in 2020 and 2021 when base rates were zero. Nobody underwrote them for a 500 basis point move in SOFR. Those vintages are the ones bleeding.

Portfolio earnings growth is also slowing. Lincoln International's data shows EBITDA growth falling from 6.5% in Q2 2025 to 4.7% in Q4. The share of companies growing earnings above 15% has dropped from 57.5% to 48.2%. Tariffs and a cooling consumer are both contributing. Not dramatic yet. But the direction is clear.

PE tells the same story. Deal value surged 57%, but deal count fell 5%. North American buyout volume dropped 7%. Fundraising declined 22%. The average fund closed at a 19% discount to target. Dry powder has never been older: over 40% has been sitting for more than two years. More than 63% of active portfolio companies in North America have been held for four years or longer. Continuation vehicles, which have tripled to $115 billion since 2020, are no longer a stopgap. They are permanent infrastructure for an industry that cannot exit fast enough.

The 401(k) wildcard

In August 2025, President Trump signed Executive Order 14330 directing the Department of Labor to open 401(k) plans to alternative assets: private equity, private credit, real estate, digital assets, and infrastructure. The DOL rescinded Biden era skepticism about PE in retirement accounts within five days.

There is roughly $11 trillion in U.S. defined contribution plans. Even a modest shift toward alternatives means hundreds of billions in new capital. Asset managers are already building the access points: 96 registered funds now offer private credit exposure and 51 offer PE.

But retail capital and illiquid assets are a dangerous combination, especially when rate uncertainty and trade policy risk can shift borrower fundamentals overnight. Blue Owl Capital recently froze retail redemptions from one of its private debt funds, opting for episodic liquidation instead. The FSOC has warned that a sustained default spike could trigger a liquidity scramble with spillover into the banking system. Retail money will flow in. The question is whether the vehicles built to hold it can survive a stress event without locking people out.

What to watch

The DOL's February 2026 guidance on 401(k) alternative asset rules. This determines how fast retail capital actually enters. Clear safe harbors for plan fiduciaries would accelerate flows dramatically.

PIK usage past 11%. This is the clearest signal of borrower stress. If it keeps climbing, more companies are deferring real cash payments on their debt regardless of what the headline default rate says.

The Fed's next move. Another 100 basis points of cuts would provide real relief to floating rate borrowers and unfreeze deal activity. A prolonged pause puts more pressure on the weakest credits and keeps the exit backlog locked up.

AI infrastructure financing. Morgan Stanley estimates private credit could fund more than half the $1.5 trillion needed for global data center buildouts through 2028. Biggest single expansion of the addressable market on the horizon, but it also brings concentration risk in a sector burning through capital with uncertain returns.

The bottom line: the growth trajectory for private markets is intact but the return profile has changed structurally. Low rates, abundant leverage, and easy multiple expansion are gone. The firms that rode the cycle will struggle. The ones with real operational depth will pull away. Being in private markets is no longer the edge. Being in the right corner of private markets, with the right manager, is what matters now.