The Market Is Pricing a Dovish Fed Chair. It Forgot About the Eleven Other Voters.

Warsh's confirmation hearing today is the easy part. What comes after is where the math breaks.

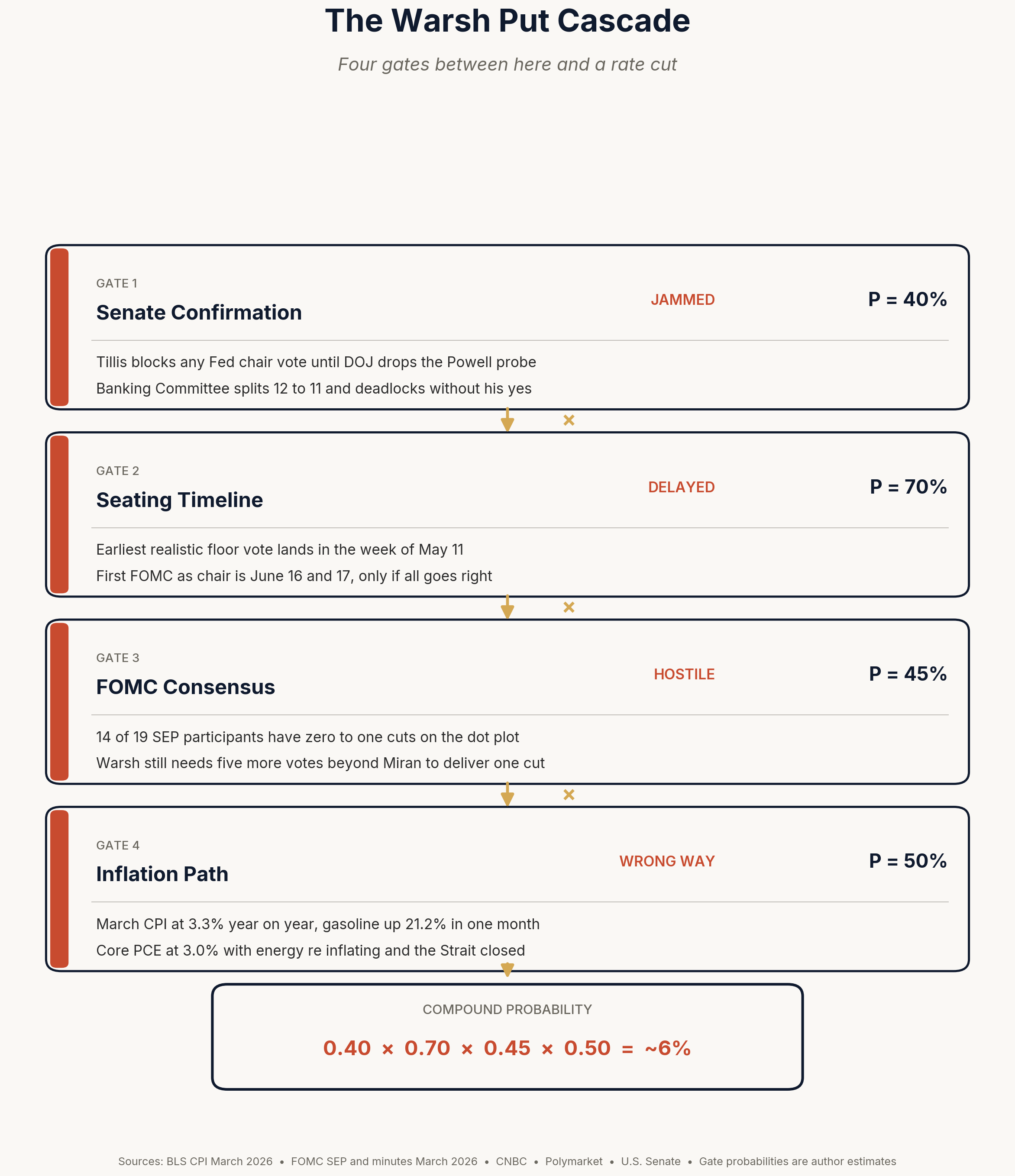

- 1Warsh is one vote on a twelve-person committee. That committee projected zero or one cuts for all of 2026 just five weeks ago. A new chair does not change the arithmetic.

- 2Tillis has said he will not vote to confirm any Fed chair while the DOJ investigation of Powell is open. The earliest a floor vote becomes realistic is the week of May 11, the same week Powell's term expires.

- 3Warsh's prepared remarks include the line 'inflation is a choice, and the Fed must take responsibility for it.' That is not what an imminent rate cutter sounds like.

What The Market Is Buying

Stocks opened near records on Tuesday. The Dow added more than 200 points at the bell. Rate futures still carry a cut for 2026. That positioning assumes Warsh gets confirmed quickly, is seated before Powell's term ends on May 15, and then persuades a hawkish FOMC to cut. None of those steps looks easy right now.

The fourth piece, inflation cooperating, is already moving in the wrong direction. The market has focused on the chair headline and underweighted the committee math and the incoming data path.

The Confirmation Math

Tillis is the bottleneck. He has said he will not vote for any Fed chair nominee while the DOJ probe into Powell tied to the $2.5 billion headquarters renovation remains open. Republicans hold a 12-11 edge on the Banking Committee, so without Tillis the nomination can deadlock and fail to reach the floor.

The Senate is out the week of May 4 and Powell's term expires May 15. The earliest plausible floor vote is the week of May 11. If Warsh is not confirmed by then, Powell can remain as chair pro tempore. The April 28-29 FOMC therefore almost certainly runs under Powell, and any rate change at that meeting remains an extreme low-probability outcome.

The FOMC Is Not A Chairmanship

The committee already told us where it stands. Fourteen of nineteen participants in the March SEP placed zero or one cut on the 2026 dot plot. The March vote was 11 to hold and 1 to cut, with Miran as the lone dissent.

Even if Warsh leans dovish in practice, he still has one vote. To move a cut through he needs five additional votes from the remaining ten voters beyond Miran. That requires clear softening in labor and inflation data, not just a change in chair rhetoric.

The Productivity Wager

The market reads Warsh as potentially dovish because of a productivity thesis: generative AI could be a large disinflationary shock that offsets sticky services inflation and energy pressure. It is a coherent argument, but the March prints have not validated it.

Headline CPI ran 3.3% year-over-year, up sharply from February, while gasoline posted a major one-month jump. Core CPI looked cleaner at 2.6%, but core PCE was already 3.0% through February and likely faces upside risk as energy passes through airfares, shipping, and food. Warsh's own framing, "inflation is a choice," sounds like a hawkish hold setup, not a near-term cut setup.

What It Means For Equities

The Russell 2000 rally is priced for cuts. If the cut path slips into 2027, that is where pressure should show first, not necessarily in the headline S&P print. Long-duration bonds face similar risk if core PCE reaccelerates and keeps real-rate pressure elevated.

At the same time, energy and defense have underperformed the index despite a backdrop that should support them. For AI-linked hyperscalers that issued large amounts of 2026 debt to fund capex, a higher-for-longer curve is a refinancing tax the market has not fully modeled.

What To Watch

Three triggers over the next six weeks should decide whether the cut trade survives.

- DOJ timeline into early May. If the probe closes, confirmation odds improve quickly. If it does not, timing pressure extends into June.

- Core PCE on April 30. A print above 3.0% with sticky services inflation takes much of the 2026 cut narrative off the table regardless of who holds the gavel.

- June dot plot direction. If the median shifts from one cut to zero, the committee has already voted against the market's productivity-led easing thesis.

The market bought the chair. It forgot to count the committee.

For informational purposes only. Not investment advice. Prices as of April 21, 2026.